As supply chain disruptions threaten to shelve some projects completely, more owners are using professional services firms to help reconfigure limited staff resources and keep schedules moving forward. In a construction market where materials shortages and cost volatility are quickly becoming the norm, firms find the most precious resource is time.

with speed to market a top priority for many project teams, professional services firms must be ready whenever owners say go, says Ron Stupi, senior vice president and COO of North American building and infrastructure for Bureau Veritas, the French power, utility and environmental services firm.

他说:“一旦预算,承包商和材料就位,我们必须准备执行。”Stupi强调,将项目组件在紧密的时间范围内一起拉动需要灵活性,或者每个人都被迫赶紧等待。他说,在最近的一项成本增长40%的项目中,所有者在选择供应商和材料方面的灵活性有助于避开供应延迟,并使时间表重回正轨。

Related Links

ENR 2022 Top 100 Professional Services Firms

ENR 2022 Top 50 Program Management Firms

View complete 2022 list, with full market analysis

(需要订阅)

“They had made commitments to financial markets and clients, but could not deliver. Our challenge was to find alternate suppliers for materials and contractors, and shift the building methods to meet their schedule,” he says. “The supply chain had many more components and moving parts to manage, creating tremendous complexity.”

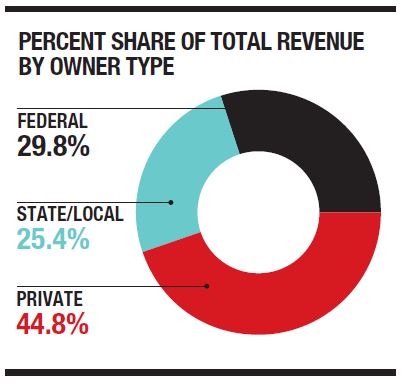

This year, revenue for 2022 Top 100 Professional Services Firms increased across the board, with total revenue up by 6.9%, domestic rising 7.2% and international revenue increasing 6.2%. Domestic revenue is still 3.4% lower than pre-pandemic levels, but firms report that owners are slowly seeking more support to manage workloads.

As owners become more risk averse in an increasingly risky construction market, companies say managing supply chain complexity will become key.

“In the short term, our industry will have to deal with a significant shortage of labor, the unmet demand for materials, and of course, inflation,” says George L. Pla, founder and CEO of Cordoba Corp., a Los Angeles-based full-service engineering firm specializing in infrastructure.

In the long term, “the main challenge is to adjust to the transition from a pandemic-era to a post-pandemic-era economy,” he says. Things won’t fully return to normal, but to “a drastically different new normal,” says Pla, and owners will need to work with professional services firms to quickly adjust.

| 排名2022 | Firm | 2021 Design Revenue in $Mil. | CM/PM-For-Fee Revenue | 总收入 |

| 1 | Jacobs, Dallas, Texas | $10,691.3 | $ 3,401.3 | $14,092.6 |

| 2 | Aecom,达拉斯,德克萨斯州 | $7,913.2 | $1,278.8 | $9,192.0 |

| 3 | Bechtel, Reston, Va. | $772.0 | $3,339.0 | $4,111.0 |

| 4 | 弗吉尼亚州Centerville的Parsons Corp.。 | $1,259.5 | $ 2,421.0 | $3,680.4 |

| 5 | Fluor, Irving, Texas | $3,519.6 | $- | $3,519.6 |

| 6 | Tetra Tech Inc., Pasadena, Calif. | $ 3,296.0 | $- | $ 3,296.0 |

| 7 | wSP USA, New York, N.Y. | $ 2,342.2 | $709.9 | $3,052.1 |

| 8 | HDR, Omaha, Neb. | $2,477.1 | $324.8 | $ 2,802.0 |

| 9 | CBRE,达拉斯,德克萨斯州 | $16.0 | $2,508.1 | $2,524.1 |

| 10 | wood, Houston, Texas | $ 2,349.8 | $- | $ 2,349.8 |

| 11 | Burns & McDonnell, Kansas City, Mo. | $2,126.4 | $183.4 | $2,309.8 |

| 12 | JLL, Chicago, Ill. | $- | $ 2,070.3 | $ 2,070.3 |

| 13 | Stantec Inc., Irvine, Calif. | $ 1,774.0 | $140.5 | $1,914.5 |

| 14 | Arcadis N. America/Callison RTKL,高地牧场,科罗拉多州。 | $1,361.1 | $ 363.8 | $1,724.9 |

| 15 | 北卡罗来纳州罗利市的金利·霍恩(Kimley-Horn) | $1,507.7 | $- | $1,507.7 |

| 16 | HNTB Cos., Kansas City, Mo. | $ 1,479.1 | $- | $ 1,479.1 |

| 17 | w或者ley, Houston, Texas | $1,397.5 | $80.1 | $ 1,477.7 |

| 18 | Gensler, Los Angeles, Calif. | $1,369.2 | $- | $1,369.2 |

| 19 | SNC-Lavalin Inc., Tampa, Fla. | $951.1 | $394.6 | $ 1,345.6 |

| 20 | Black & Veatch, Overland Park, Kan. | $ 1,226.7 | $115.0 | $1,341.6 |

Managing Roles and Revenues

looking ahead, Top 100 execs see opportunities for professional services firms to increase market share, especially in the areas of design and construction.

Of this year’s Top 100 firms, 91 firms had higher revenue this year than last year’s equivalently ranked firms. Median revenue increased 7.45%, to $46.85 million, from $43.6 million reported last year.

with increasing role distinctions placed on construction management (CM) versus program management (PM), CM revenue numbers are now parceled out to examine short- and long-term trends (see chart, p. 57). Total CM revenue is $7.72 billion.

下午总营收增加5.73%至162.3亿美元this year, from $15.35 billion last year. Domestic revenue rose 2.94%, to $11.53 billion, and international revenue increased 13.01%, to $4.69 billion, from $4.15 billion last year.

对于许多公司,与分包商和供应商的合作伙伴关系对于在当前市场条件下的能力和保持竞争力至关重要。

On top of what IPI owner and President Kevin Ball calls a “rigorous subcontractor pre-qualification process,” he says that “the current market has encouraged us to focus more intently on our relationships with engineers, suppliers and contractors.”

The firm brings partners in earlier for value engineering as well as to optimize schedule and materials availability.

“Today, our conversations with clients focus more on project planning and delivery options to deliver the best results in the current environment of labor and supply chain shortages,” says Ball.

Capacity and financial strength are more important than ever when selecting subcontracting partners, firms say. Partners need tangible resources to navigate supply chain issues, and firms need to be flexible to attract top talent.

“拥有大型团队的项目的所有新利18备用网址者不能足够迅速地工作,尤其是考虑到我们正在经历的紧张劳动力市场,”卡明首席人物Scott Weaver解释说。“当客户曾经在寻找一到两名全职员工的地方,我们被要求提供四个或更多。”

weaver says that he sees the trend continuing over the next three years. “Until owners have worked through their backlog of projects, they are putting increased pressure on the market and demand for top talent,” he adds.

| 排名2022 | Firm | 2021年收入$ 000 $。 | 设计收入为$ MIL。 | CM/PM-For-Fee Revenue in $Mil. | 总收入为$ MIL。 |

| 1 | 弗吉尼亚州雷斯顿的贝克特尔。 | $12,953.0 | $772.0 | $3,339.0 | $ 17,064.0 |

| 2 | Aecom,达拉斯,德克萨斯州 | $ 6,270.1 | $7,913.2 | $1,278.8 | $15,462.1 |

| 3 | The Turner Corp., New York, N.Y. | $14,283.1 | $- | $162.9 | $14,445.9 |

| 4 | Jacobs, Dallas, Texas | $- | $10,691.3 | $ 3,401.3 | $14,092.6 |

| 5 | Fluor, Irving, Texas | $8,810.2 | $3,519.6 | $- | $12,329.8 |

| 6 | Kiewit Corp., Omaha, Neb. | $10,679.3 | $996.0 | $- | $ 11,675.3 |

| 7 | STO Building Group Inc., New York, N.Y. | $9,510.0 | $- | $- | $9,510.0 |

| 8 | 马里兰州巴尔的摩的Whiting-Turner Construction Co. | $8,353.5 | $- | $12.3 | $8,365.9 |

| 9 | DPR Construction, Redwood City, Calif. | $ 7,491.7 | $- | $- | $ 7,491.7 |

| 10 | Skanska USA, New York, N.Y. | $6,371.8 | $- | $162.3 | $ 6,534.1 |

| 11 | Clark Group, Bethesda, Md. | $ 6,295.4 | $- | $- | $ 6,295.4 |

| 12 | Gilbane Building Co., Providence, R.I. | $ 6,074.8 | $- | $ 125.2 | $6,200.0 |

| 13 | PCL Construction,丹佛,科罗拉多州。 | $6,046.3 | $- | $- | $6,046.3 |

| 14 | Tutor Perini Corp., Sylmar, Calif. | $5,938.7 | $- | $- | $5,938.7 |

| 15 | Hensel Phelps, Greeley, Colo. | $ 5,510.0 | $- | $- | $ 5,510.0 |

| 16 | The Walsh Group, Chicago, Ill. | $ 5,272.7 | $- | $- | $ 5,272.7 |

| 17 | Clayco, Chicago, Ill. | $ 4,984.0 | $- | $- | $ 4,984.0 |

| 18 | 密苏里州堪萨斯城的JE Dunn Construction Group。 | $4,917.9 | $- | $- | $4,917.9 |

| 19 | Holder Construction, Atlanta, Ga. | $ 4,906.0 | $- | $- | $ 4,906.0 |

| 20 | Mortenson, Minneapolis, Minn. | $ 4,830.8 | $- | $ 7.1 | $4,837.8 |

Infrastructure Influx

Alfred Mackey, PFES senior vice president of operations and strategy, believes that 2022 will be a redux of 2021 “regarding access to capital and managing materials constraints.”

“我们(策略)自2012年以来已经建立trong and dynamic partnerships across industries,” he says. “Due to the influence the coronavirus had on the global marketplace, we have continued to mature our procurement strategies and build progressive relationships relationally as well as have production slots within international manufacturers.”

2021年Redux的一部分不是1.2亿美元的基础设施投资和就业法案,该法已成为该行业对有限资源的竞争的X因素。

公司预计,公共机构将需要更多的第三方专业服务公司来帮助他们管理工作量。但是,即使是没有完成与基础设施支出相关的工作的公司也在为整个市场的活动激增做准备。

IPI is not currently in the public infrastructure market, “but we do expect that activity to put additional pressure on industry supply chains and labor availability, both at the management and craft levels,” says Ball.

Anser Advisory CEO Bryan Carruthers expects growth in third-party agency CM and PM to continue as owners of capital projects and programs are faced with staffing issues and will need to turn to consultants to assist across the program lifecycle.

“We’ve seen strength across sectors within the Southern California market where infrastructure projects have been in the works even prior to federal funding due to [the] 2028 Olympics,” he points out. “We have also seen strong demand for services within aviation nationally after a slight slowdown due to COVID-19 and across other transportation sectors.”

The infrastructure funding law “will undoubtedly lead to a greater volume of federal and state programs and projects to pursue,” says Bryan Ritch, marketing director at PMA Consultants LLC. But “timing and location of funding could prove challenging for strategic planning,” he says.

Ritch继续说:“我们正在与当前的基础架构客户沟通,并研究其他需求,以准备增加工作。”

Staffing the programs and projects is another challenge for professional services firms,” he says. In his opinion, the “spending bills are extensive in their scope” but “vague on understanding the federal, state and local funding distribution process and channels.”

At Hill International, the company is being asked to increasingly take on an advisory role for agencies in its core transportation business sectors of roads, rail, bridges and aviation.

“We are talking to them about how they can mature their organizations and prepare for the [infrastructure law] money,” says CEO Raouf Ghali.

Agreeing with the assessments of many other Top 100 firm executives, he says he also believes that supply chain delays are here to stay—at least “for a little while longer.”

To avoid industry-wide bottlenecks, professional services firms will need to be equally pragmatic when it comes to phasing for program management and construction management projects. Says Ghali: “The sheer amount of funds that may be coming down in such a short time is not something that has been seen for quite a few decades.”